A Brief History of Electronic Payments

Before cards, chips, and phone taps, there was barter. People traded what they had for what they needed: grain for tools, salt for cloth, livestock for labor. It worked fine in small communities, but imagine trying to pay your barber with two chickens. Barter depended on coincidence: finding someone who wanted exactly what you had and who owned exactly what you wanted. Eventually people realized that value itself could be represented by something portable and trusted.

And that's when money appeared. At first, it was whatever everyone agreed was valuable: shells, pieces of copper, or polished stones. But around the 7th century BCE, something remarkable happened near the coast of modern Turkey. In Ephesus, worshippers of Artemis began using small stamped pieces of electrum – a natural alloy of gold and silver – as tokens of value. The nearby Lydian kingdom took the idea further. They stamped coins with the image of a lion, the royal symbol of power, to guarantee authenticity. This was more than a clever trick. It turned money into a promise: whoever accepted that coin could trust what it was worth.

From Lydia, coinage spread like wildfire. Greek city-states refined the designs, Rome industrialized them, and later empires built their economies on those little pieces of metal. Even India's and Persia's earliest coins carried traces of that same idea—value backed by authority. China's coins developed separately, but the principle was the same: create a small object that people could trust.

Centuries later, merchants and rulers discovered a lighter form of money: paper. Imperial China had already experimented with it by the 9th century. By the Renaissance, European traders were carrying handwritten bills of exchange—basically IOUs – I Owe You's – that crossed borders faster than wagons of silver ever could. Money was no longer metal; it was information.

The next leap came with banks and central currencies. By the 17th and 18th centuries, banks issued notes backed by reserves, and governments established national currencies to unify trade. The industrial era brought checks, telegraph transfers, and clearing houses... all mechanical precursors to digital transactions. Every stage was about the same thing: making the exchange of value faster, safer, and less physical.

Then, the electronic age began.

1950s – Birth of the Credit Card

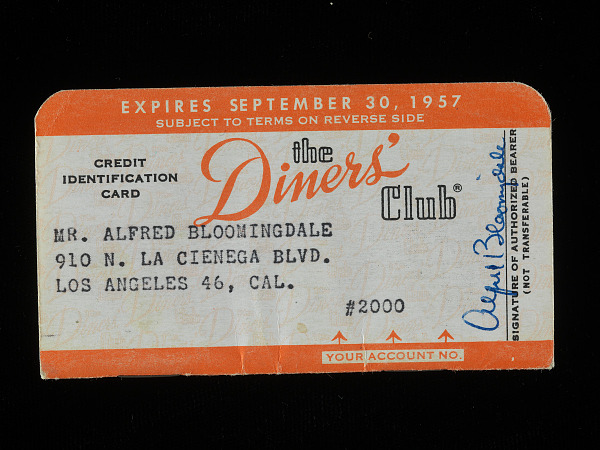

In 1950, Diners Club launched something no one had seen before: a card that didn't pay instantly, but later. It was made of cardboard, accepted at just a few dozen restaurants, and mainly used by well-dressed businessmen who didn't want to carry cash to lunch. Within a year, 20,000 people had joined. For the first time, paying and spending were no longer the same moment. You could dine today, sign a slip, and worry about it next month.

A few years later, Bank of America took the concept to the masses. In 1958, it mailed out 60,000 unsolicited BankAmericards in California — a marketing stunt that caused chaos, fraud, and unpaid bills, but also ignited a revolution. That card would later become Visa. By 1966, other banks wanted in, forming Master Charge, the network that would evolve into Mastercard.

For consumers, it felt like magic. For banks, it was a gold rush: credit, data, and loyalty, all in one piece of plastic. The modern idea of "financial convenience" was born.

1960s-70s – Going Plastic & Going Global

If you think your metal Amex or titanium card feels fancy, remember that the first "cards" were literally paper. By the 1960s, plastic took over: sturdier, cleaner, and easier to machine-print. Mass production meant millions of people could finally carry one.

But with growth came trouble. Fraudsters learned to copy embossed numbers and signatures. To fight back, IBM engineers invented the magnetic stripe in the late 1960s: A small black strip that could hold encrypted account data. Now machines, not humans, could verify transactions.

This era also introduced the ATM, the automated teller machine. Suddenly, banks had 24-hour reach, and people could withdraw cash at night without seeing a single teller. Around the same time, the first electronic POS terminals arrived. Before that, merchants used mechanical imprinters (nicknamed "knuckle-busters") to make carbon copies of card numbers.

By the late '70s, terminals could connect directly to banks via dial-up. What used to take minutes of paperwork now took seconds over a phone line. Each small leap — plastic cards, magnetic stripes, electronic approvals — pushed payments closer to what we'd later call digital commerce.

1980s-90s – The Digital Age Dawn

As computers got faster, payments followed. Debit cards joined credit cards, linking directly to checking accounts. For the first time, everyday transactions moved from paper to silicon. Then came the Internet. In 1994, the first secure online purchase took place. As the tales tell, someone bought a Sting CD. So 1994. Four years later, a small company called PayPal appeared, allowing people to send money over email.

It's hard to overstate how revolutionary that must have felt. Until then, "online payment" meant typing your card into a web form and hoping it worked. PayPal made it instant, peer-to-peer, and global. Looking at PayPal's 1999 design reminds me how early web interfaces looked overcrowded and uncertain. Yet, they set the stage for the fintech boom that would follow.

Meanwhile, fraud kept pushing innovation. Banks introduced EMV chips (named after Europay, Mastercard, Visa) to replace the easy-to-clone magnetic stripe. The new system generated unique cryptograms for each transaction, and chip-and-PIN became the European standard.

Around this time, MOTO (Mail Order / Telephone Order) became the go-to method for remote payments. Before websites and online checkouts existed, customers phoned or mailed their card details to merchants, who entered them manually through terminals. It was the original Card-Not-Present channel — the ancestor of e-commerce — and it's still used today in hotels, travel agencies, and call centers. Because there's no card or customer present, MOTO transactions always carried higher fraud risk. They also sit outside modern rules like 3D Secure and Strong Customer Authentication (SCA), which is why some older or hybrid e-commerce setups are still technically processed under MOTO contracts to bypass those requirements. It's convenient, but risky: no authentication means no liability shift if fraud occurs.

As fraud from remote payments increased, issuers looked for a simple way to prove a buyer actually had the card in hand. Enter the CVV — Card Verification Value. First introduced by Mastercard in the mid-1990s, it's the small three- or four-digit number printed on the back (or front for Amex). The CVV isn't stored in the magnetic stripe or chip; it exists only on the card, so even if a database of card numbers is stolen, the attacker can't easily make online purchases. It was a tiny addition that became one of the most effective security checks in card-not-present payments.

2000s – Secure Online Payments & Mobile

The early 2000s brought 3D Secure (Verified by Visa, Mastercard SecureCode, etc.), adding an authentication step to online card payments. Mobile phones became payment devices, first through text messages and then through smartphone apps. To tackle rising fraud, PCI DSS (Payment Card Industry Data Security Standard) was established in 2004, defining how payment data must be stored and transmitted. In 2024, the latest version 4.0.1 was released, continuing that evolution.

By the late 2000s, contactless NFC payments let people pay by simply tapping a card or phone. Digital wallets (PayPal, Alipay, WeChat Pay), peer-to-peer apps (Venmo), and buy-now-pay-later services (Klarna, Afterpay) reshaped consumer behavior. In 2007, the first iPhone arrived, but it wasn't until 2014 that Apple Pay launched, followed by Google Pay in 2018.

And then regulators entered the chat. Europe's PSD2 directive, rolled out around 2018, made two-factor authentication mandatory for most online payments. Friction, perhaps — but necessary. In return, it also opened the door for Open Banking, allowing new apps to move money directly between accounts. For consumers, checkout became nearly invisible. Think Uber: you never "pay", it just happens. A simple booking on your app, and your funds move. It's not just about technology. It's about removing every trace of effort from the act of paying.

2020s – The Present

Then came a global pause. The COVID-19 pandemic changed how we shop and pay. Stores stopped touching cash. People tapped cards for everything, and e-commerce grew faster in months than it had in years. Contactless limits rose, and even small merchants joined the digital wave. Today, we're seeing the rise of real-time payments (instant bank transfers), the experimentation with central bank digital currencies, and the steady march of biometrics. Fraud detection now runs on machine learning models that can score a transaction faster than you can blink.

It's an exciting, strange, slightly terrifying time. Payments have become a background process: always on, always watching, rarely failing. And yet, the principle hasn't changed since those early Lydian coins: trust. Every advancement, from metal to mobile, was just another way to make that trust easier to share. Who knows... a fully cashless society or alternative-based payments might be around the corner.