Alternative Payment Methods

Cards may be the most recognized way to pay, but they are far from the only one. Around the world, people use an incredible variety of payment methods — many designed around local habits, regulations, and technology. This guide explains the most common types in a nutshell, giving you the context behind how and why people pay differently across markets.

For a complete directory of payment methods and their details, check out the full Payment Methods Overview.

Digital Wallets

Digital wallets such as Apple Pay, Google Pay, and Samsung Pay take the traditional card and virtualize it inside your phone. Instead of presenting your physical card, your device creates a tokenized version that's used to authorize payments.

This approach not only improves security but also changes the experience entirely. A fingerprint or facial scan replaces your PIN or signature, and your credentials never leave the device. Behind the scenes, Apple and Google work with card networks to ensure the same infrastructure handles these tokenized transactions as regular card payments. For many consumers, digital wallets are now the preferred way to pay: fast, safe, and contactless, both online and in-store. It's my preferred way of paying honestly. Couldn't imagine a world without tapping my phone every day.

Local Wallets

Then there are local wallets, which dominate specific regions. Think Twint in Switzerland, MobilePay in Denmark, Vipps in Norway, WeChat Pay and Alipay in China. Unlike global wallets, these apps usually connect directly to local bank accounts rather than cards. Payments move through domestic clearing systems, often instantly and with minimal fees. This makes them highly efficient within their home markets.

Many of these wallets have expanded beyond payments into messaging, loyalty, or peer-to-peer transfers, effectively becoming part of daily life. In some countries, a QR code on your phone is all you need to pay for anything from a taxi ride to your morning coffee.

Loyalty and Reward Schemes

Not all payment instruments are purely financial. Some come wrapped in rewards. Loyalty programs and co-branded cards blend payments with incentives such as cashback, airline miles, or shopping points. While they might not seem like "payment methods" in the strictest sense, they influence how people choose to pay.

Supermarket chains, airlines, and even coffee shops run loyalty ecosystems that connect directly to payment systems. Some use physical cards, while others link rewards to your phone number or digital ID. The goal is to make paying more than just a transaction — it becomes part of a brand relationship.

Invoices and Buy Now, Pay Later (BNPL)

In countries like Switzerland, Germany, and across the Nordics, invoicing remains one of the most traditional yet enduring ways to pay. Instead of being charged immediately, customers receive an invoice after their purchase and settle it within 30 days. This method, deeply ingrained in local consumer habits, is still widely used for online shopping, utilities, and even healthcare. It reflects a cultural norm of trust between buyer and seller — the idea that payment comes after the product or service is received.

Building on that idea, Buy Now, Pay Later (BNPL) services such as Klarna, Afterpay, and Twisto have brought the concept into the digital age. They let shoppers split payments into installments right at checkout, while the BNPL provider immediately pays the merchant in full. The result is a kind of modern credit system without the formality of a credit card — fast, frictionless, and highly appealing to younger consumers who value flexibility and instant gratification.

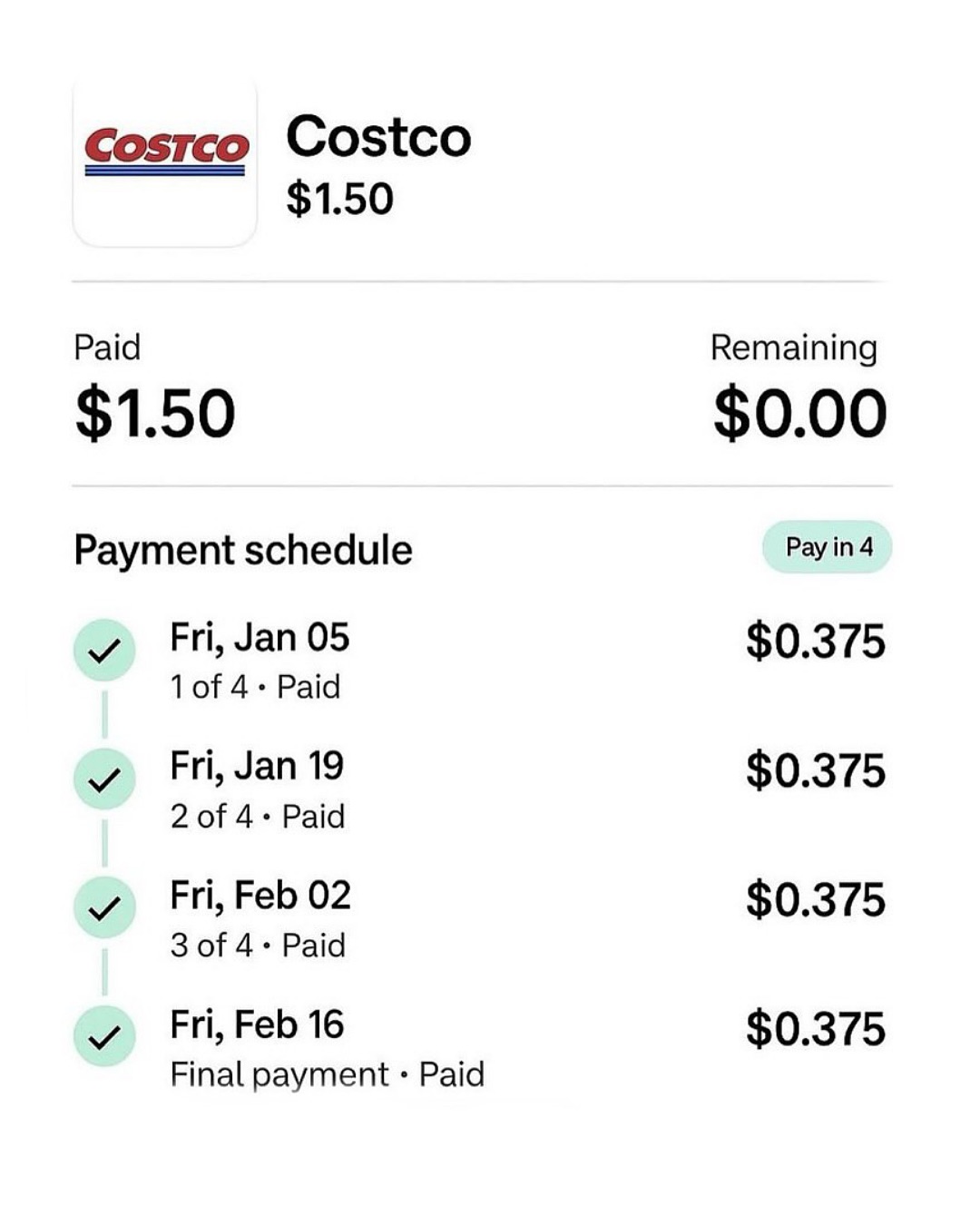

BNPL reach has grown so wide that it now shows up in unexpected places. Costco, for instance, started accepting BNPL purchases — and yes, someone had to actually buy a $1.50 hot dog combo and proudly paid it off over three months for the meme. It's absurd, but also telling: deferred payment has become so convenient and normalized that it's no longer about affordability, but habit. What began as a trust-based invoice model has evolved into a global ecosystem of micro-credit, embedded directly into the checkout experience.

Yet this convenience comes with a cost. Many young consumers are discovering that the same ease of splitting payments can quietly lead to overspending and debt accumulation. With multiple BNPL plans running in parallel across different apps, it becomes surprisingly hard to keep track of what's owed and when. Studies in several markets have shown rising delinquency rates among BNPL users, suggesting that easy credit can make financial discipline harder, not easier. What feels like freedom at checkout can turn into a subtle form of financial dependency later. Anyway, I'm still a big fan of Klarna and their services.

Gift Cards and Vouchers

Finally, we have gift cards and vouchers — often underestimated but incredibly widespread. Products like Paysafecard or prepaid shopping vouchers let consumers pay online without sharing bank details. For merchants, they help reach unbanked users or those wary of entering card details online. Gift cards also serve as marketing tools and closed-loop payment systems. A retailer might issue a gift card that works only in its own stores or apps, creating both convenience for the customer and loyalty for the brand.

Payment methods have diversified massively. Cards laid the foundation, digital wallets redefined convenience, local wallets embedded payments in culture, loyalty programs added emotion, and new models like BNPL and vouchers expanded inclusion. For merchants, supporting the right mix of methods is no longer optional — it's essential. Every market has its own favorites, and understanding them is key to building trust and maximizing conversion.