Important Card Payment Topics

Cards are deceptively simple. You tap, insert, or type a number, and the rest just happens. But behind that moment, a handful of mechanisms make recurring payments, tipping, and even multi-installment purchases possible. Let's look at a few of them.

Tokenization — Keeping Card Data Safe

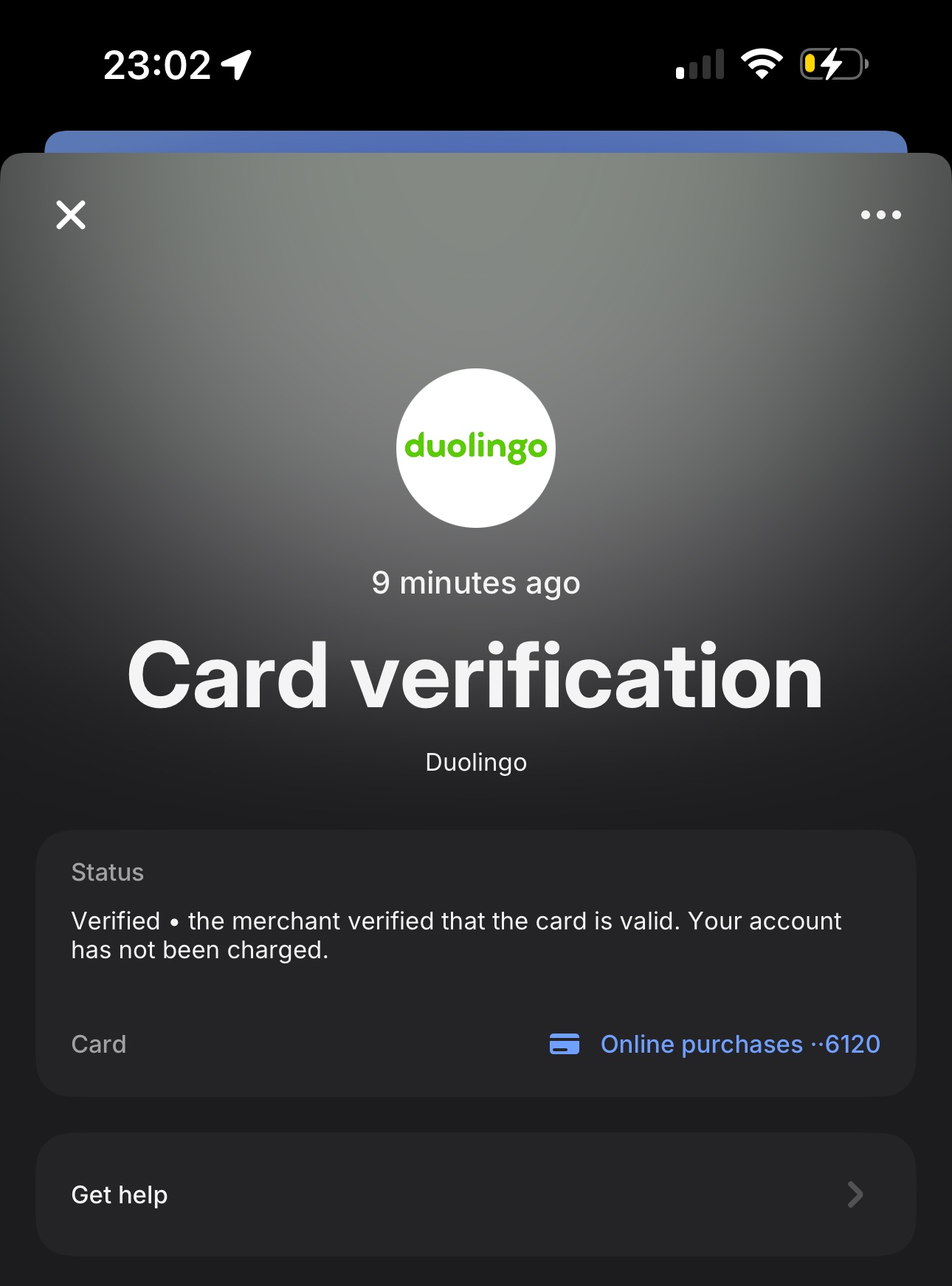

When a card is stored for future use — say, for a subscription, recurring billing, or one-click checkout — the merchant doesn't actually keep the real card number. Instead, it's replaced by a token: a unique identifier that can only be used within that specific environment. Before they can safely store that token, merchants often perform a card verification — a small, temporary authorization that confirms the card is valid before saving it for later use.

Gateway or service tokens, provided by payment service providers (PSPs) or specialized security firms such as PCI-Proxy.com, allow merchants to handle card data securely without ever storing it themselves. These companies tokenize sensitive card details the moment they're captured, returning a safe reference — the token — that can later be used for payments, refunds, or subscription renewals. No payment is actually authorized during this process; it's a "tokenization-as-a-service" model designed purely to keep merchants out of PCI DSS scope while preserving payment flexibility.

Tokens can originate from different sources. Some PSPs issue and manage their own proprietary tokens within their gateway, meaning those tokens can only be used within that specific ecosystem. Others rely on independent tokenization providers such as PCI-Proxy, which operate as neutral intermediaries. These services can link to multiple acquirers or PSPs, giving larger merchants the freedom to route transactions across providers while maintaining compliance — all without ever touching real card data.

Finally, some issuers and card networks generate post-authorization tokens, created after a successful payment to enable future captures, refunds, or recurring charges without re-entering the full card number. Each approach differs in timing and ownership, but they share a single purpose: to let merchants operate efficiently while keeping cardholder data safely abstracted, encrypted, and well out of reach of prying hands.

Network Tokens and Account Updater

Network tokens take tokenization one step further by moving it inside the card networks themselves. Instead of a PSP or merchant generating a token, the scheme (Visa, Mastercard, American Express, etc.) issues it directly and links it to the real card behind the scenes. This means the token isn't tied to a single merchant or gateway — it's portable across multiple PSPs that support the same network tokenization framework.

The biggest advantage is automatic lifecycle management. When a customer's physical card expires, is lost, or reissued, the underlying token stays valid. The card network simply maps the token to the new PAN. This prevents failed charges due to outdated card data — a major source of declines in recurring payments and stored-credential transactions.

Working alongside network tokens are Account Updater services. These are automated systems operated by issuers and schemes that notify acquirers or PSPs whenever card details change. Instead of the merchant discovering an "expired card" error at the next billing cycle, the PSP receives an update and refreshes the stored data proactively. In practice, the two systems complement each other:

- Account Updater fixes data before the next billing attempt

- Network Tokenization removes the dependency on card changes entirely

Together, they quietly improve approval rates, reduce customer churn in subscriptions, and make "card on file" payments far more resilient to real-world events like renewals, reissues, and card replacements. This is rather a newer topic and not many PSPs offer this functionality.

Subscriptions and Hosted Recurring Payments

Recurring billing may sound simple — "charge the customer every month" — but it hides a lot of logic: retries, dunning, failed renewals, and regulatory nuances like SCA exemptions for recurring transactions.

Some payment providers, such as Stripe, offer hosted subscription systems that manage this entire lifecycle. They handle scheduling, retries, invoicing, and even customer-portal management. Others expect you to build the logic yourself, only exposing APIs for storing cards or initiating charges.

Hosted subscriptions simplify compliance and reduce development overhead, but they also mean surrendering some control over timing and messaging. For larger merchants, custom recurring setups still make sense — especially when linked to complex invoicing or account management systems.

Paying in "N Times" — Installments and Local Traditions

In some markets, paying in several installments isn't an exception; it's the norm. France's "paiement en 3 fois" or "4 fois" lets customers split a purchase into equal payments directly at checkout. The first installment is charged immediately, the rest automatically on the agreed schedule.

In Mexico, banks and schemes like Visa and Mastercard support "Meses sin Intereses" — interest-free monthly installments often promoted by retailers and card issuers. The merchant gets paid upfront by the acquirer, while the issuer collects from the consumer over time.

These installment products are technically card transactions, but they follow specific scheme rules and local clearing logic. For customers, they make large purchases manageable; for merchants, they increase conversion — especially for high-value goods.

Tips, Gratuities, and Donations

Payments aren't always about the exact price of a product. Many systems include an optional step to express appreciation or generosity.

At POS, this means a tipping screen — a fixed percentage, round-up option, or manual entry before final confirmation. Hospitality and service industries rely heavily on these flows, which are defined by local regulation (in some countries, tips can't be pre-added or must appear separately on the receipt).

Besides tip, a similar idea powers donations and round-up programs, where customers can add a small amount to support a cause. From a technical standpoint, these are usually additional authorization amounts or separate follow-up charges, but the experience feels seamless.

Whether it's rewarding good service or funding a social project, tipping and donations remind us that not all payments are purely transactional — sometimes they're emotional.