Fees & Fund Distribution

Ask any merchant what they pay for payments and they'll probably shrug. They might say "around two percent", but the truth is rarely that simple. Every electronic payment involves a handful of players — each taking a small, mostly invisible share — and what's left is what the merchant finally receives. Let's unpack that web and follow a single €100 payment from the customer's pocket to the merchant's account.

The Illusion of Clear Fees

Payment pricing looks simple on paper: "2.9 % per transaction". In reality, that rate is a blend of multiple components — interchange, scheme, acquirer, and sometimes gateway fees — bundled into one neat figure. It's measurable, yes, but rarely transparent. The actual fee can depend on things like:

- card type (credit, debit, premium, corporate)

- transaction channel (in-store or online)

- country combinations (domestic or cross-border)

- the merchant's business category.

So when you read "2.9 %", it might already include a dozen micro-fees beneath the surface. The acquiring contract (next chapter) explains how those layers are structured — but for now, think of it as a dinner bill split among several guests, each paying for their part of the meal.

The Fee-Takers

Every transaction is a small ecosystem of value exchange. The issuer (the consumer's bank) takes an interchange fee, usually around 0.2 % – 0.3 % for debit and 0.3 % – 0.5 % for credit cards in Europe. It's their reward for taking risk, managing fraud, and providing the card. The card network (Visa, Mastercard, etc.) charges a scheme fee to route and regulate the transaction. It's small — typically €0.02–€0.10 per transaction, sometimes with an added fraction of a percent for cross-border payments. The acquirer (merchant's bank or PSP) keeps a margin for processing, risk coverage, and settlement. Often between 0.2 % and 0.5 %, depending on volume, risk, and contract terms. The gateway usually charges a fixed authorization fee, like €0.05 per transaction, and sometimes a monthly platform fee or extra cost for fraud screening. Put together, these slices make up what merchants call the Merchant Discount Rate (MDR) — the total cost of card acceptance.

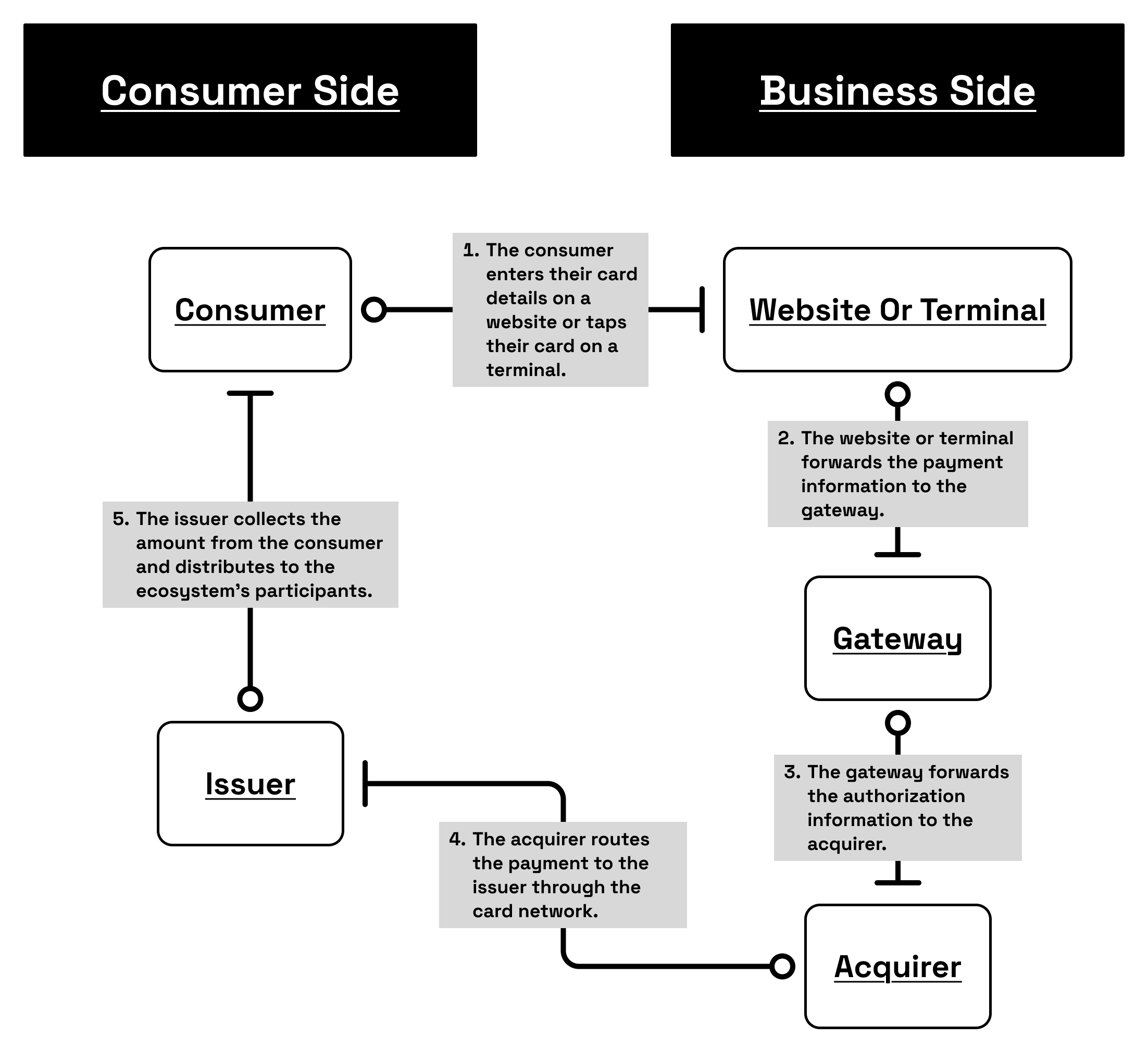

Let's imagine a customer buying a pair of shoes for €100.00, either in an online shop or at a physical terminal. It feels instant — one tap, one click — but behind that small gesture, a chain of messages travels through multiple systems in less than a second.

- The customer pays €100.00 — The moment the button is pressed on a merchant's website or the card is tapped on a terminal, the payment gateway takes charge. It encrypts the payment details, wraps them into a secure authorization message, and sends them to the acquirer — the merchant's bank or payment processor.

- The acquirer forwards the request — The acquirer doesn't decide if the transaction should go through; it simply forwards the authorization to the right card network (Visa, Mastercard, etc.). Think of the acquirer as the merchant's representative inside that global chain.

- The card network routes it to the issuer — The issuer, the customer's bank, checks the request: Is the card active? Are there enough funds? Does the pattern look normal? If everything checks out, it sends an authorization approval back through the same chain — issuer → network → acquirer → gateway → merchant — all in roughly 300 milliseconds.

- The funds aren't transferred yet — What's happened so far is a promise: the issuer has reserved €100 on the customer's account, waiting for the merchant to capture it later. Only during settlement (usually one to three business days later) does the actual money move.

Now, when the €100 finally flows from the issuer to the acquirer, each participant takes their cut:

- Issuer (the customer's bank) keeps its interchange fee — let's say 0.30 % (€0.30) — for providing credit, risk management, and fraud protection

- Card network charges a scheme fee, around €0.10, to cover the cost of maintaining global rails and rules

- Acquirer deducts its margin — typically 0.25 % (€0.25) — for processing, compliance, and settlement

- Gateway or PSP charges a fixed tech fee, often €0.05, for running the API connections, tokenization, and dashboards

| Component | Fee | Amount (€) |

|---|---|---|

| Consumer pays | – | €100.00 |

| Issuer (Interchange) | 0.30 % | 0.30 € |

| Scheme (Card Network) | – | 0.10 € |

| Acquirer (Margin) | 0.25 % | 0.25 € |

| Gateway (Fixed) | – | 0.05 € |

| Total fees | – | 0.70 € |

| Merchant receives | – | €99.30 |

This breakdown is a figurative example, meant to illustrate how fees are split rather than define a fixed standard. Actual costs vary widely by region, card type, and especially by industry. In many low-risk sectors, paying around 0.7 % in total fees is indeed a bargain — but in higher-risk areas such as adult entertainment, gambling, or crypto, processing fees can climb sharply, sometimes reaching several or even double-digit percentages. Acquirers often also hold rolling reserves (e.g., 10 % of revenue for 180 days) as added protection.

So although the issuer authorized €100, the merchant only receives €99.30 after all fees are settled. These numbers are average examples — the real cost depends heavily on who you are and what you sell. Large retailers or airlines can negotiate lower fees because of their high volumes and low risk, while smaller or higher-risk industries — like gambling, travel, or crypto — pay more. That's partly because of their Merchant Category Code (MCC), a four-digit identifier used by networks to classify business types and apply the corresponding fee structure.

But Cash Isn't Free Either

Cash feels free because no statement shows a line for it. But handling cash costs money too — counting, reconciling, depositing, insuring, even guarding it. A supermarket moving hundreds of thousands in notes every week spends hours of staff time and often pays bank deposit fees or armored-transport costs. And that's before you factor in shrinkage — theft, errors, or fake bills. Once you compare those hidden costs to a digital fee of 0.7 %, cards start looking like a bargain.